The Software Slaughter

Why the Best Software Isn’t Being Disrupted -- It’s Being Mispriced

I. The Slaughter

The AI Revolution, as Dan Ives often calls it, has been characterized by fast-paced, relentless, heavy-hitting innovation. When all three show up at once, they can crush like a middle linebacker in the gap. And the software sector appears to have been standing flat-footed.

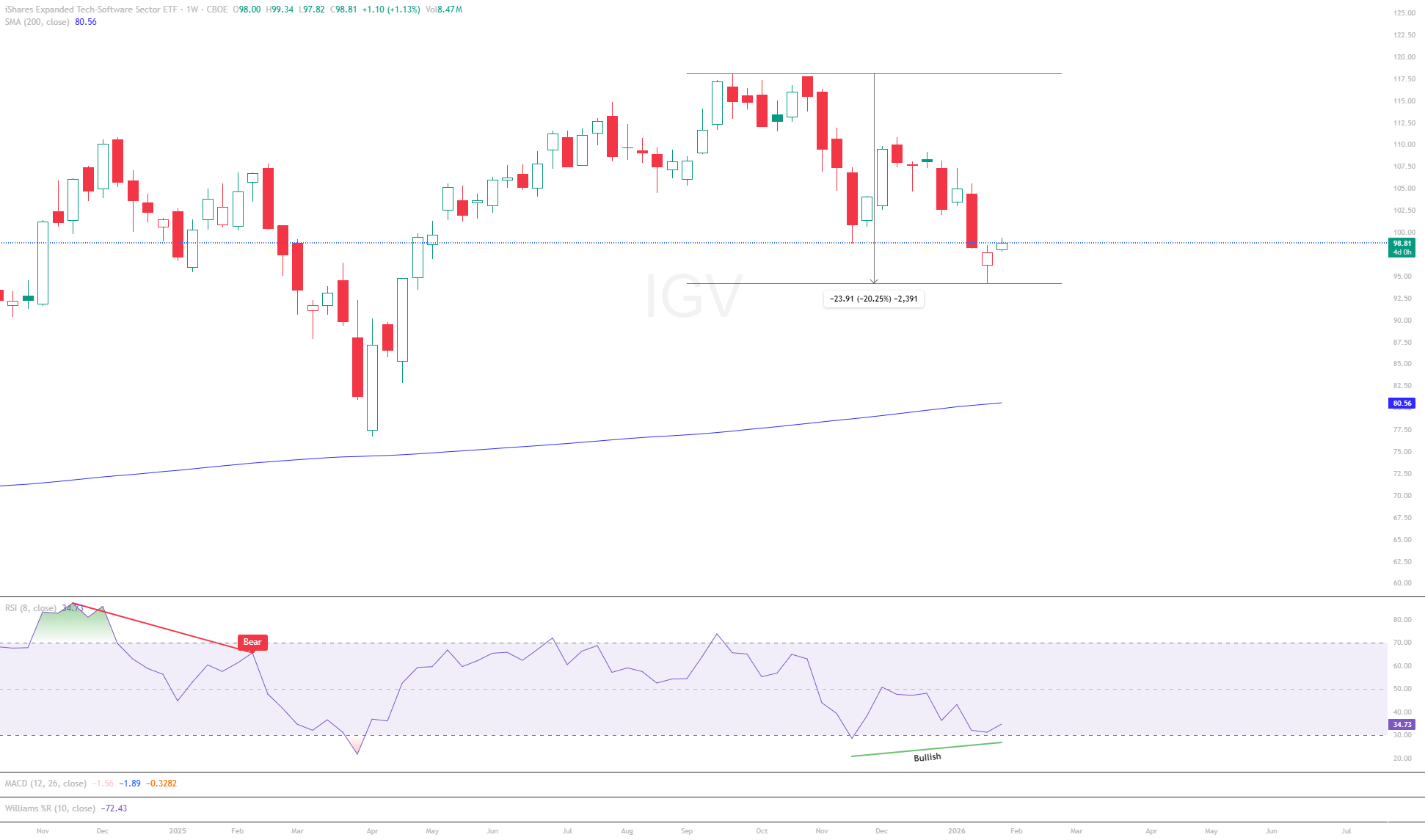

The iShares Expanded Tech-Software Sector ETF IGV 0.00%↑ was down roughly 20% from its highs just days ago, even as the S&P 500 SPY 0.00%↑ and NYSE churned to new highs alongside strong market breadth. While the Qs have lagged, failing to make a new all-time high for roughly 85 days, the NASDAQ 100 advance/decline line made a new high about a month ago, potentially foreshadowing further upside as we head into a heavy earnings window. Regardless, IGV’s price action has clearly diverged from the broader market.

This divergence matters. Markets don’t do this without reason, but they also don’t always discriminate correctly.

II. The False Narrative

Fears around AI disruption, particularly agentic AI, have shocked the software sector and driven a full-scale de-rating. Wall Street has done what it often does best:

Shoot first and ask questions later.

Major constituents have been hit hard (peak-to-trough):

Microsoft MSFT 0.00%↑: -20%

Salesforce CRM 0.00%↑: -40%

Oracle ORCL 0.00%↑: -45%

Adobe ADBE 0.00%↑: -55%

ServiceNow NOW 0.00%↑: -45%

CrowdStrike CRWD 0.00%↑: -20%

But these sell-offs are not all created equal.

Adobe, for instance, has been under pressure and limping for over a year. What’s changed recently is that blue-chip enterprise software, names like Microsoft, ServiceNow, and CrowdStrike, have been swept into the same bucket. In effect, software has become a macro trade.

The dominant fear is straightforward:

AI increases productivity

Productivity reduces headcount

Fewer employees mean fewer seats

Seat-based SaaS revenue models break

Layer on top of that a second concern, that new AI-native products are so innovative and inexpensive to deploy that they outright replace legacy SaaS platforms, and you get what markets are currently pricing: structural demand impairment.

The problem with this narrative lies in its assumptions about enterprise behavior.

Large enterprises and Fortune 500 companies do not move like startups. They are not agile enough, nor incentivized, to swap out deeply embedded platforms, rewrite workflows, retrain employees, and re-architect systems on the fly. Software is not just installed; it is trained. Employees are trained on software. Software is trained on enterprise data. Workflows and processes are institutionalized over years, sometimes decades.

To expect a company like JPMorgan to simply drop a platform such as ServiceNow, which is woven directly into enterprise workflows, in favor of a disruptive point solution is naïve. The cost, risk, and operational friction of such a move are enormous.

This reality highlights the distinction the market is currently missing: there is a difference between fragile software and foundational platforms. And in an era of rapid AI innovation, the winners are unlikely to be replaced by AI, they are more likely to be the vehicles through which AI is delivered to the enterprise.

Technical Context (Brief, by Design)

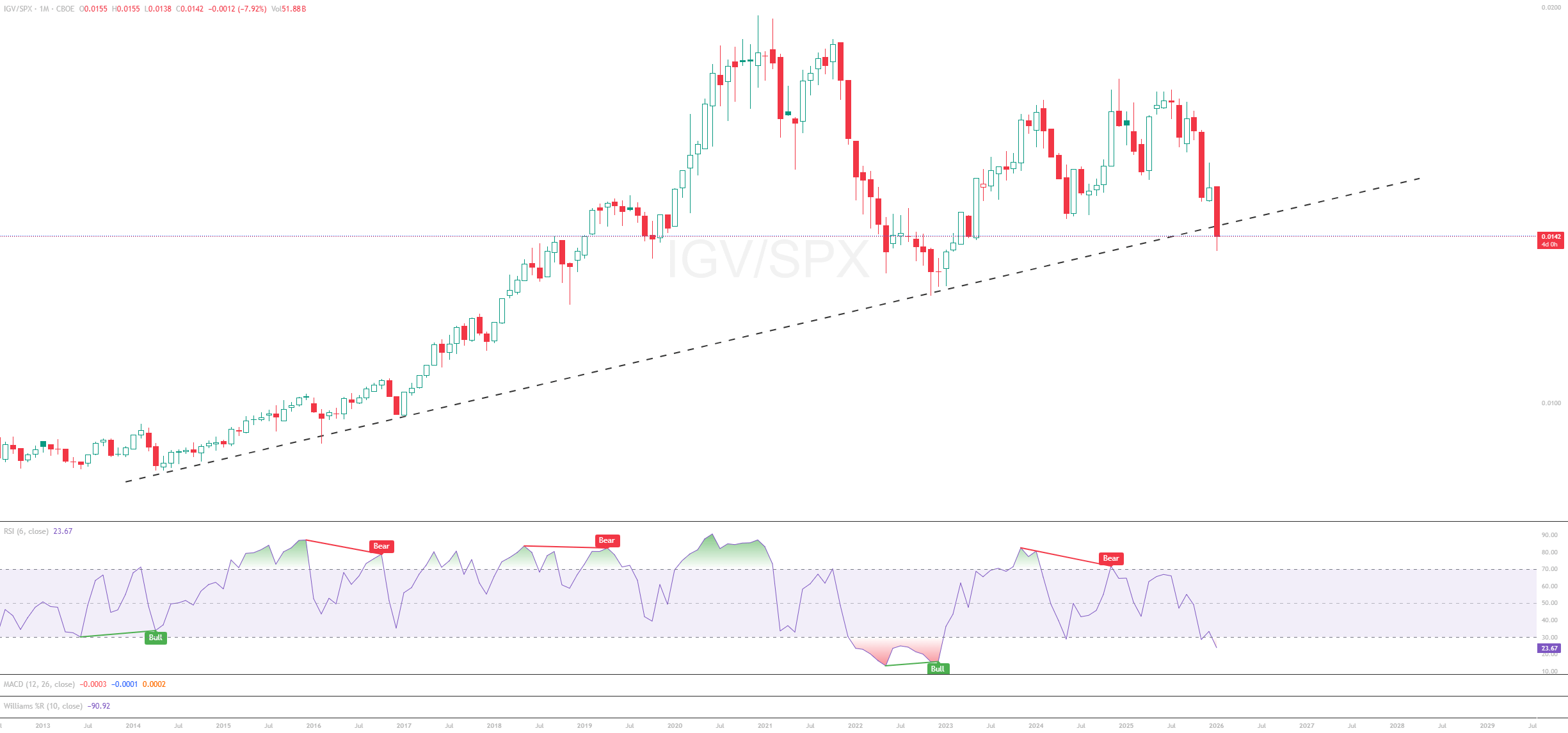

I won’t bore you with ten IGV charts and pages of technical analysis (follow me on X @L1amBellamy if you want that), but one chart is worth sharing: IGV relative to the S&P 500 on a monthly basis.

IGV has recently tested and briefly undercut a relative performance trendline that has held since 2014. At the same time, monthly RSI(6) is oversold for only the third time in roughly 20 years, a rare condition that historically aligns with long-term opportunity. I use RSI(6) on the monthly timeframe because, contextually, it captures roughly half a year of price action.

While I believe the software sector broadly represents opportunity, I do not believe all software will recover equally. AI disruption will create clear winners and losers. As a result, stock selection within IGV may offer far better risk-reward than owning the ETF outright, where one may end up “diversifying away alpha.”

That is why my focus is on software businesses where AI, and agentic AI, are features, not bugs.

III. Why ServiceNow Is Not “Just Another SaaS”

In picking software stocks, there is one name that has stood out to me: ServiceNow NOW 0.00%↑.

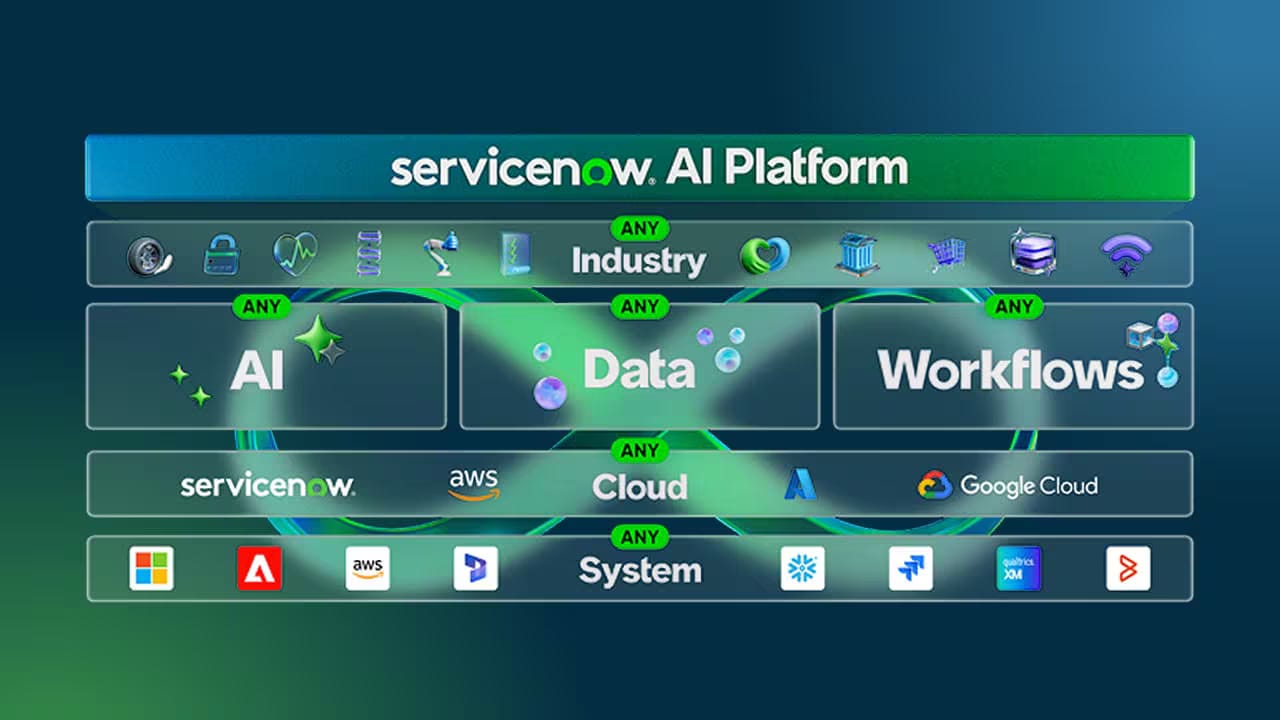

ServiceNow is a provider of IT service management and workflow automation at the enterprise level. But that description undersells what the company actually does. ServiceNow unifies large organizations across IT, HR, sales, operations, security, and more into a single system of record for enterprise workflows. This matters, especially for large enterprises, because work does not happen in silos. It moves across departments, permissions, approvals, and systems.

This is the key distinction the market is currently missing. ServiceNow is not a point solution. It is not a “nice-to-have” productivity tool. It is infrastructure - plumbing at the enterprise level. It is where work gets routed, approved, logged, audited, and executed. Large enterprises do not rip out workflow engines lightly.

That embedded nature is the foundation of ServiceNow’s durability.

IV. Leadership in a Period of Disruption

ServiceNow is led by CEO Bill McDermott, who has decades of experience across Gartner, SAP, and ServiceNow. In periods of rapid technological change, leadership matters, and McDermott is one of the company’s greatest assets, even if that asset does not appear on the balance sheet.

McDermott has navigated enterprise software transitions before. In the early 2010s, SAP faced a real risk that cloud-native competitors would undercut its high upfront license pricing and push its core systems to a passive, back-office role, with innovation happening elsewhere. McDermott responded by pushing the company to abandon its legacy license-first model in favor of subscriptions, retraining sales teams, resetting customer expectations, and reshaping the platform so SAP remained the system enterprises built through, not around. The company not only survived the transition but grew its market value from roughly $40 billion to $160 billion in the process. That playbook directly applies as AI pressures seat-based SaaS pricing and challenges the relevance of traditional software models. When disruption accelerates, experience compounds, and there are few software veterans better suited to lead an enterprise platform through an AI-driven transition than Bill McDermott.

V. The Numbers Speak for Themselves

The financial and operating metrics tell a remarkably consistent story.

ServiceNow has grown revenues at 20%+ for a decade. Customer renewal rates have remained roughly 98% for a decade. Remaining performance obligations (RPOs) have continued to grow at a steady clip. Since its IPO, the stock is up approximately 2,600%.

These are not the characteristics of a fragile business. Take another look at those renewal rates.

Nearly 8,400 organizations, including more than 85% of the Fortune 500, trust ServiceNow to run critical workflows. That install base is the real asset. Revenue growth is simply the output.

Gartner reinforces this positioning. In its 2025 Magic Quadrant for AI applications in IT service management, ServiceNow sits in a quadrant of its own. Notably, Moveworks, previously positioned as a challenger, has since been acquired by ServiceNow, further consolidating leadership.

VI. Agentic AI Is a Feature, Not a Bug

ServiceNow is my favorite play in software precisely because agentic AI is a feature, not a bug.

The prevailing fear is that AI will replace SaaS platforms outright. That logic breaks down at the enterprise level. Large organizations don’t adopt intelligence in isolation; they adopt systems that embed intelligence into workflows. AI models need permissions, workflow routing, auditability, governance, and integration with legacy systems. That is where ServiceNow lives.

ServiceNow has leaned directly into this reality. The company recently announced a multi-year partnership with OpenAI, expanding customer access to frontier models. OpenAI models will be a preferred intelligence capability for enterprises running more than 80 billion workflows each year on ServiceNow’s platform.

This reinforces ServiceNow’s role as the AI control tower for business reinvention. Models think. Platforms act.

ServiceNow is the medium through which agentic AI actually becomes enterprise output.

I simply do not believe large enterprise clients will abandon deeply embedded platforms in favor of standalone AI tools. It is not feasible operationally, financially, or culturally.

VII. The Seat-Based Fear and the Pricing Transition

Another major concern weighing on software valuations is the idea that AI-driven productivity gains will reduce overall headcount, shrinking the number of seats purchased from SaaS vendors.

It’s a reasonable assumption, though not one that is objectively underway at scale yet, and ServiceNow has already moved to address it.

The company is actively shifting toward a hybrid pricing model, particularly for its AI-driven Now Assist products. This model complements traditional seat-based subscriptions with consumption-based pricing, billing based on actual AI actions or “assists” rather than raw headcount.

This approach allows ServiceNow to monetize work performed, not just people employed.

There are real risks here. Most AI-related revenue today still comes from subscription uplift rather than true usage-based consumption. Converting pilots and early adoption into sustained, scalable consumption will take time. Large organizations don’t move quickly, and integration complexity and workflow friction could slow that transition.

But that risk is already reflected in the stock. ServiceNow is down roughly 45% from its all-time highs. This is not a timing play. it’s a time play. Narrative repair happens quarter by quarter, not overnight.

VIII. Inorganic Growth: Moveworks and Armis

ServiceNow has also been proactive on the inorganic front, announcing two major acquisitions: Moveworks and Armis.

Moveworks strengthens ServiceNow’s front-end capabilities, combining agentic AI and automation with enterprise search and conversational interfaces. With thousands of AI agents already deployed, the acquisition accelerates enterprise adoption across growth areas including CRM. If agentic AI is supposed to kill SaaS, ServiceNow is again ahead of the curve, integrating it directly into the platform.

Armis expands ServiceNow into cyber exposure management and cyber-physical security across IT, operational technology, and critical infrastructure. The deal, priced at roughly 23× ARR, has drawn scrutiny. That’s fair - it’s not cheap.

But strategically, it makes sense. Cybersecurity is non-discretionary, demand continues to grow, and security workflows fit naturally into ServiceNow’s platform DNA. The acquisition allows ServiceNow to offer a unified, end-to-end security exposure and operations stack that can see, decide, and act across the enterprise.

This is the double-edged sword ServiceNow faces. Avoid acquisitions and risk being labeled flat-footed or obsolete. Invest aggressively and be criticized for overpaying. In both cases, the company is punished.

Yet the direction is consistent: ServiceNow is building the platform that delivers AI, securely, governably, and at scale, to the enterprise.

IX. Valuation and Technicals

From a valuation standpoint, ServiceNow is revisiting levels that have historically mattered.

Forward P/E is re-testing a low last seen in early 2023. Given the current backdrop - public sector budget pressure, concerns around SaaS demand impairment, scrutiny around recent acquisitions, and broad fear around disruptive AI - it is at least worth asking whether the market has already priced in a meaningful portion of the bad news. While there is certainly a world where multiples compress further and break below this range, it is notable that the stock has begun to catch a bid at these levels. Whether this ultimately proves to be a floor remains to be seen, but it is a level that demands attention.

Forward price-to-free-cash-flow tells a similar story. The multiple is once again testing a zone that has previously acted as support and held. Importantly, this is not an uncharted valuation regime for ServiceNow, we have been here before. What’s different today is not the multiple, but the narrative framing. AI is being treated as an existential threat to software platforms rather than a force that must ultimately be absorbed and operationalized by them.

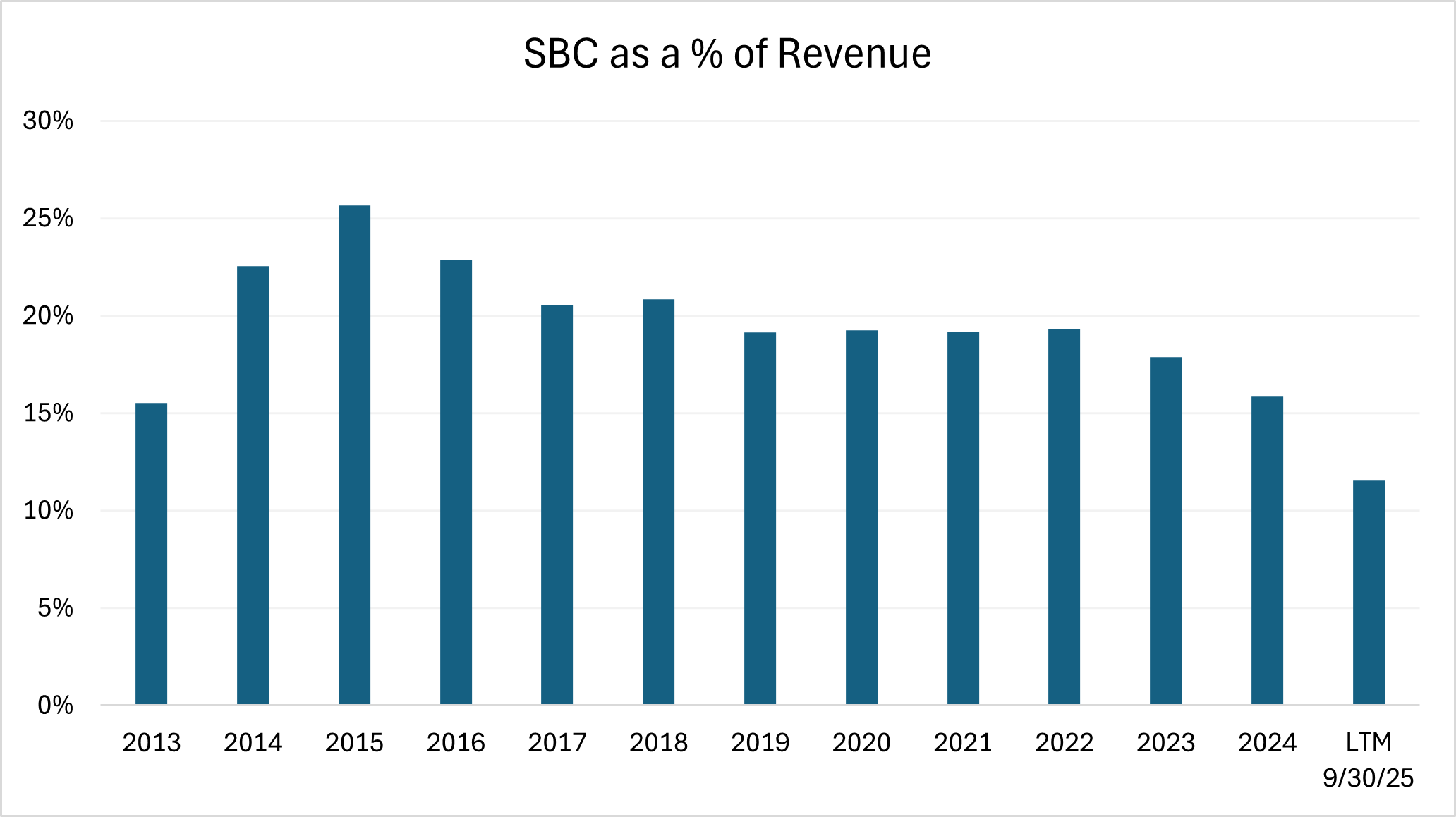

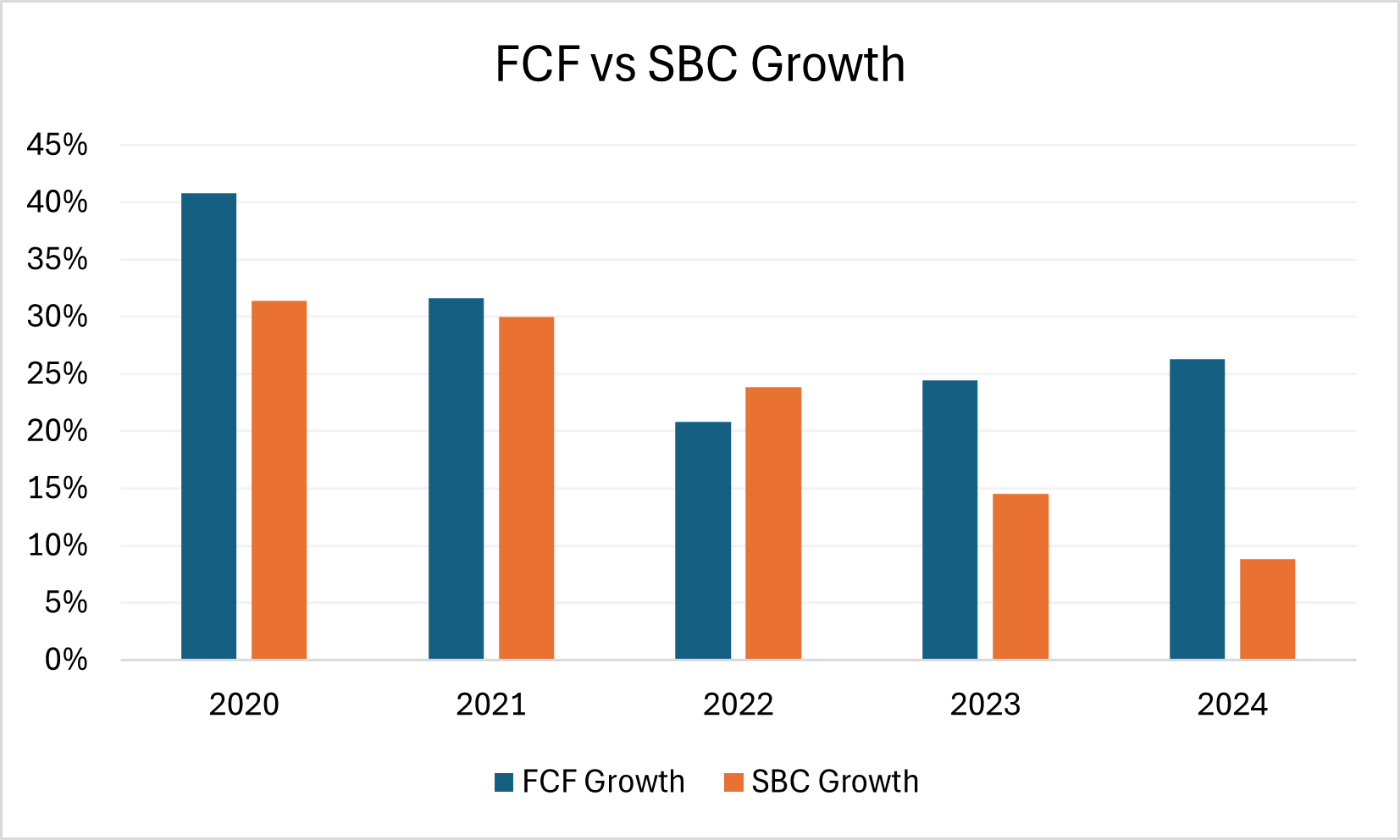

Stock-based compensation (SBC) is often cited as a risk for software companies, but the trend matters more than the headline number. At ServiceNow, SBC is not a new feature of the business… it has existed throughout the company’s entire growth cycle. What has changed is its intensity. Over time, SBC has steadily declined as a percentage of revenue. That signals discipline, not excess. In other words, while absolute SBC has grown alongside the business, it has become less dilutive on a relative basis as ServiceNow has matured and expanded margins.

While SBC is a real cost through dilution, the more relevant question for shareholders is whether it is being outpaced by value creation. Over time, ServiceNow’s free cash flow growth has consistently exceeded (except 2022) the growth in SBC over the past 5 years, indicating that incremental cash generation has scaled faster than equity issuance. Comparing growth rates helps illustrate whether dilution is earning its keep. In this case, it is.

The technical picture reinforces the overall bullish setup.

While I personally spend most of my time on the daily and weekly timeframes, I prefer to zoom out for pieces like this, which are meant to resonate with long-term investors. On a higher timeframe, the stock is revisiting a well-defined support/resistance zone and found support quickly after briefly undercutting it. I would be constructive on a monthly close within or above this zone.

Notably, when price did dip below support, it found footing near an area of heavier volume, as shown by the anchored volume profile from November 2021. That suggests prior participation and potential long-term interest at these levels. At the same time, RSI (6) is in an oversold condition, only the third time in the stock’s history this has occurred. Historically, that setup has rewarded patient investors, even if not immediately.

To be clear, further downside is absolutely possible. Earnings are tomorrow, and the market will be watching renewal rates, growth trajectories, and early signals around AI monetization closely. Volatility should be expected. That said, earnings also represent a potential inflection point: another quarter of stable renewal rates, margin expansion, and continued revenue and RPO growth could begin to shift the narrative and serve as a catalyst for the bull case.

That said, the confluence between valuation multiples reverting to prior floors and technicals reaching historically oversold conditions is compelling. It doesn’t guarantee an outcome, but it does suggest the risk/reward has meaningfully shifted compared to where it stood a year ago.

X. Other Ways to Play It

Other ways to gain exposure to this theme include the broad software index, iShares Expanded Tech-Software Sector ETF, or selectively owning key constituents within the index, most notably Microsoft, the #1 holding, and CrowdStrike, currently the #10 holding.

CrowdStrike is particularly attractive given the stickiness of its platform and the non-discretionary nature of cybersecurity spend. Cybersecurity remains one of my highest-conviction themes as the world continues to digitize, expand attack surfaces, and increase reliance on connected systems. I’ve written about CrowdStrike before, and I encourage readers to revisit my April 2025 article for a more detailed overview. It has been and will continue to be a staple of my digitalization-oriented portfolio.

Microsoft needs no introduction. It offers software exposure through a Mag 7-quality balance sheet, unmatched distribution, and a dominant position across enterprise software, cloud, and AI tooling, and it currently trades well below its highs. For investors who want software exposure with scale, durability, and optionality, Microsoft remains a straightforward way to express that view.

The reason I highlight these names, rather than recommending a full allocation to IGV, is the “Expanded” nature of the ETF itself. I question some of the holdings within IGV. Names like MicroStrategy and BitMine Immersion (snake oil salesman) skew closer to crypto exposure than true enterprise software. Others, such as Palantir, operate in a world of their own, leaning heavily toward government and defense applications and carrying what I view as elevated valuation risk.

This isn’t a knock on Palantir, its investors have been well rewarded, but 110× sales is not my cup of tea. I’m more than happy to strip the basket down to Microsoft, ServiceNow, and CrowdStrike to get pure, blue-chip exposure to enterprise software at a time when the market appears uninterested.

As the saying goes:

“The only place in the world where people run from a sale is markets.”

I’ve learned that a sound process can still produce losing outcomes in the short run. That doesn’t invalidate the process. Losing is apart of winning. The edge comes from building a framework you trust, and having the patience to stick with it when the outcome hasn’t caught up yet.

I don’t write often. I write when conviction demands it. Calling for a Bitcoin bear market at the highs was considered crazy. Buying high-quality software platforms down 30–50% is considered crazy too.

But markets routinely overshoot narratives, especially during periods of technological transition. I may be early, and I may endure drawdowns, that’s the price of stock picking, but durable, free-cash-flowing platforms on sale are exactly where long-term opportunity tends to hide.